Fear, uncertainty and doubt has worked well for many incumbents in the technology and online media game over the years. Why should sell-siders be any different when it comes to Agency Trading Desks (ATDs)? Don’t worry…they’re not.

With buy-siders generally tight-lipped about the subject of ATDs, the resulting vacuum is being filled by constant industry sniping and chatter. Since the advent of the ATD, they have had aspersions notoriously put on them – perpetuating FUD. That the industry trade media and blogs are the only place that a consistently negative view of ATDs can be found should come as no surprise. Yet, the recent spate of chicken-little articles, posts and heated comments represent what is apparently a really threatened sell-side point of view.

Double-dipping. From the best defense is offense school. It is as if the basic math around billable hours and the service-layer around managing Demand Side Platforms have no value. Data-driven media buying is very different from traditional demo-driven index based methods and takes alot of time as clients and agency partners get up to speed. Moreover, the measurement planning, analytics, technical and media accounting and media reconciliation that are required to manage these campaigns are also very different.

The notion of “double-dipping” belies a basic misunderstanding of the process: DSPs are not exactly push-button. It is nothing like an in-house production studio – it is very strategic not simple production. Leveraging the expertise associated with intricate technical aspects of tags and data sources alone is a significant effort. Also as a reminder, digital advertising used to be commissionable or marked-up like traditional media. Meanwhile, where is the outrage at ad networks double-dipping with advertiser data?

Profit-margins. The implication that agencies shouldn’t be seeking profitable service offerings is simply outrageous. In the end, it is a service business and comprised of talented specialists that care about client business. With the prevalence of small-scale site retargeting making up alot of the business today, the ad volume and associated fees that ATDs are charging suggest that they may be running somewhat in the red; at least, until the business scales up or broadens to warrant the resource investment.

Advertisers squeezing too hard here run the risk of running the people (not machines) doing the work into the ground – not good either. ATDs are not charitable organizations so it is not clear why they should be expected not to earn fees or why they have to justify it ad nauseaum. That said, it is in ATDs best interest to be very transparent with clients about the fees they are charging.

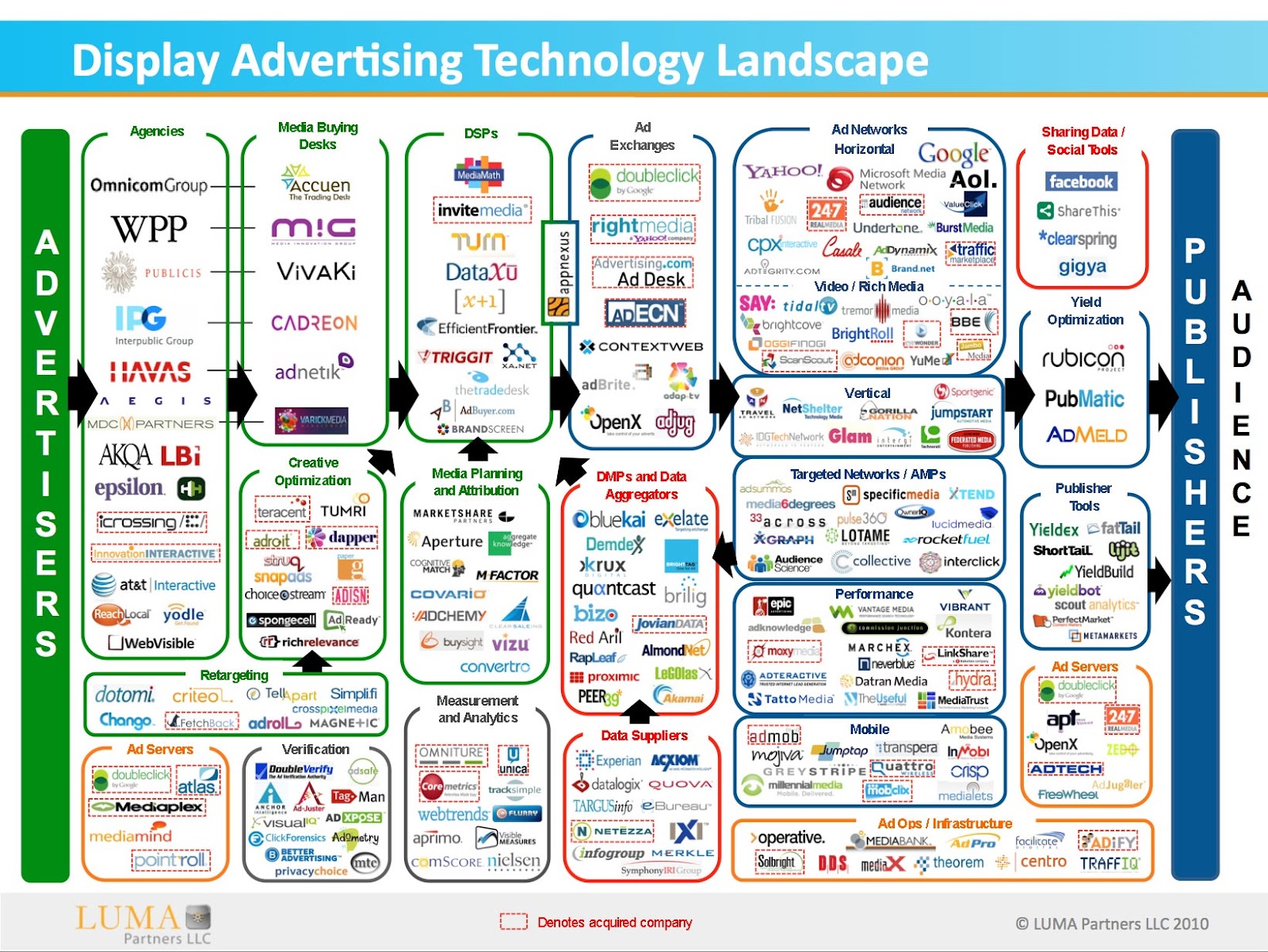

Agency Technology Investment. Holding company ATDs, for the most part are not building their own buying technologies in-house. The spin-out of Adnetik being an exception and who’s success remains to be seen. Instead they are licensing DSP tools/white-labelling and applying their tech-savvy marketing teams to enable a platform for the benefit of clients. While their marketing often use the term platform, they mean technology and the service-layer to support it – not literally hardware and software.

In some cases, agencies may be using their business intelligence tools to support ATD reporting – that makes sense and is nothing new. Agency analytics teams have been using home-grown BI for years. Advertisers really just need to ask their agency questions if they don’t understand how all of it works…this recalls a famous Chinese proverb: He who asks a question is a fool for five minutes; he who does not ask a question remains a fool forever.

Data-hoarding ATDs. Really? The sell-sider rhetoric on this point is very misleading. Most ATDs are essentially service-providers, consultants armed with a DSP SLA (service level agreement) and the expertise. While agency BI tools attempt to provide handy storage of performance data (with debatable proficiency). Historical benchmarks and campaign reporting data are not the same as actionable behavioral user-level data, i.e. cookies. No, afraid that data is sitting inside ad networks, ad servers (which, by the way sometimes turns out to be the same cookie used by the ad exchange) or in a Data Management Platform.

Now that said, there is simply no excuse for an ATD or agency to clandestinely re-purpose

so-called 4th party data from ad campaigns for later use. That is a major ethical lapse and sell-siders (publishers) should not tolerate. Ironically though, at the same time, far too many major ad networks are happy to re-purpose advertiser and publisher campaign performance data when it can maximize their revenue.

Mandate. Just what are sell-siders so afraid of? Perhaps their advertiser clients getting the most experienced and savvy teams working on their behalf and more transparancy. That is a huge benefit for client-side marketers that remarkably all too often have few senior digital media natives in-house. As a result, there is a huge-learning curve and time means money in a service business.

The flip-side is that an agency holding company not consolidating their technical and negotiating expertise on one team raises management competency questions. With the level of technology change today, a centralized team is exactly what holding companies should be doing to effectively manage their resources. A better question and especially so for site retargeting is, that ad networks are still being considered. If old-school planner-buyers are concerned then they ought to put in for a transfer to the ATD.

Conflict of Interest. Wow – look at who is talking. Most advertisers would probably prefer the dedicated separate team within their ATD (usually closely directed by their agency-of-record) than what naked and supposedly independent sell-siders and technology vendors have to offer to protect their interests, i.e. nothing. It seems no different than a client directly buying from a media vendor, where that really new “big idea” has actually been shopped to several other advertisers (probably not all that new.) Plus, if an advertiser decides to pass, 100% probability that “idea” will be offered up to an advertiser’s competitor. Hey, clients can certainly pay a premium for category exclusivity – that option is always available.

On the other hand, AORs by definition get the concept of category exclusivity. With ATDs, there is semblance of brand stewardship and a compeitive firewall. Moreover, an ATD’s media planning agency partners are very unlikely to put any one client account at risk. That’s because in game theory terms, branding is a zero-sum game, i.e. it is about brand X winning, which means that brands A, B and C lose. As such, the ad strategies that are successful cannot be shared, nor the ones that didn’t. The problem is that sell-siders and technology vendors often have the opposite – industry specialists.

The Machine Knows Better. Of course it makes sense to leverage automatic optimization and novel algorithmic approaches to improve results. However, far too many of the sell-siders and arms vendors out there purport that an ATD just can’t keep up. That may or may not be true but consider the source. How many sellers are transparent enough to report on the performance of their supposed-machine learning technologies? Some will do it but only when asked.

In any case, marketers will always have a need to explain and justify their actions. The client-side CFO does not want to hear about magic or blackboxes. They want to understand how to allocate cash to generate ROAS and ROI in a predictable way. People can be held accountable in a way machines cannot. The simple fact is that advertisers need expert brains to adjust to the changing marketplace and resources – managing campaigns on their behalf.

Early-in-session User Performance. One of the more clever rhetorical devices that pops up when sellers realize they are about to get disintermediated. It essentially questions the competition’s inventory quality suggesting that either directly or indirectly that only they have access to the special ad inventory. That’s right, through first dibs or exclusive relationships, the seller’s inventory “performs better” and therefore more valuable than the other. It is possible but depends on the seller’s definition of perform – for their bottom line or for their client’s? BTW, still waiting for the data or performance reports that back-this up after multiple requests. Ironically, most of these sellers are also getting a portion of their inventory from the same exchange sources as the ATD; the real question is just how much.

Simplistic Wall Street Metaphors. This is an oldie…first of all day-trading media is a very one-dimensional way of viewing media consumption. It is not the same as a financial asset that has intrinsic value (stocks, bonds, options)…however it does make for nefarious and ominous metaphors with the recent financial crisis and all. Digging past the hackneyed writing, RTB by definition doesn’t allow positions to be taken in the same way as financial trading. These are real-time transactions, i.e. a spot market where ATDs aren’t owning inventory or taking a position. It seems that there is a fundamental misunderstanding of financial atribitraging.

It seems like the amount of technology required to squeeze out any kind of profit through exploiting information inefficiencies across many RTB decisions is more likely going to come from a DSPs that can hedge across multiple advertisers. ATDs just don’t have the financial structure, engineering or research staff to pull this off. In practice, this is nothing more than another red herring. Any ATDs that could save client’s big money would want that to be known.

Kick-backs. One of the more outrageous charges about kickbakcs was refuted in public and so the matter should be closed. Yet, the meme continues to proliferate. It may also depend on the definition of a kick-back. Is free user training or better support a kick-back? How about box seats to the Cubs game and fancy meals? Without knowing the internal accounting between DSPs, exchanges and ATDs it may never be known for certain. Clients can always ask for audit rights but like all memes this one can be difficult to prove or disprove.

Did I miss any or do you have any others to add? Feel free to submit a comment below!